Australia’s new merger clearance regime went live on 1 January 2026 and it’s a game changer for M&A in Australia. Both local and international dealmakers need to rethink strategy, timing and risk, as ACCC notification is now mandatory for certain acquisitions linked to Australia, even where there’s no competitive overlap.

Here’s what you need to know, now.

10 Key Aspects of the New Regime

- The regime is mandatory and suspensory for notifiable deals, with the ACCC as the primary decision maker.

- The types of acquisitions covered are far broader than under the old regime.

- Notification thresholds are low and apply even if there is no competitive overlap between the buyer and seller, with a 3-year lookback.

- A notification waiver process is offered by the ACCC for low-risk deals. This is largely a public process.

- Detailed, very prescriptive up-front information requirements mean huge front-end effort by merger parties.

- Fixed mandatory timelines for ACCC determinations are a positive, but are subject to clock stops and extensions.

- Substantial and cumulative filing fees depending on transaction value are payable on filing and even if a deal falls over. It’s a user pays system.

- Transparency and publicity has increased due to the ACCC’s acquisitions register and ACCC decisions being published.

- With limited exceptions, there is no confidential review of deals by the ACCC outside of pre-notification engagement. The ACCC routinely expects engagement ahead of filing for all deals.

- There can be no notification without deal certainty (eg. heads of agreement, preferred bidder status), but the ACCC can consider waiver applications where an acquirer is actively engaging in a competitive bid process. Whether this exists is a question of fact.

When is ACCC notification required?

From 1 January 2026, notification is required for an acquisition of shares or assets if:

1. The shares or assets to be acquired are connected with Australia; [1]

2. The acquisition of shares or assets meets any of the notification thresholds in Table 1;

3. For an acquisition of shares, immediately after the acquisition is put into effect:

- the acquirer (including its associates) obtains control of the target body corporate, or

- the acquirer doesn’t obtain control [2] but its voting power meets one of the voting power thresholds in Table 2; and

4. No exemption is available[3] or no waiver has been granted by the ACCC.

Significant penalties apply if a transaction requiring notification is not notified to the ACCC before completion. Further, the transaction is void.

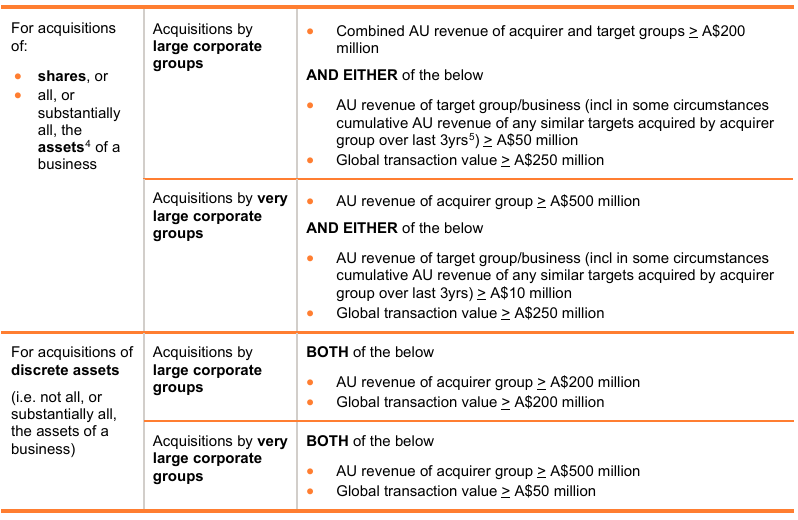

Table 1: Notification Thresholds

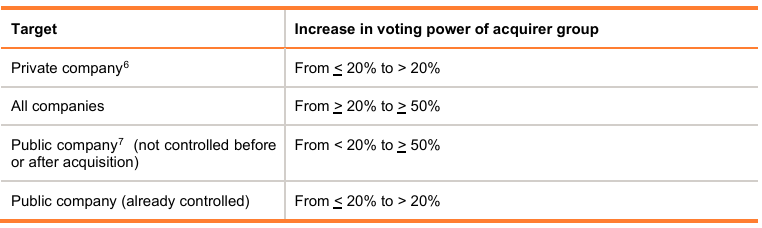

Table 2: Voting Power Thresholds

What are the practical implications for deals?

Higher compliance costs + risk for more deals: The new regime creates new legal and commercial risks and higher compliance costs for a wide range of transactions outside of classic “M&A” deals. The stakes are high as failure to notify can void transactions and lead to significant penalties.

Deal strategy must change: Buyers and sellers must assess merger risks early, every time, at the front-end of deals, to understand the implications for deal timing and deal execution.

More seller risk + buyer scrutiny: With more deals caught, the ACCC not reviewing multiple competitive bids and no confidential clearance being possible, sellers may need reverse break fees, and divestiture commitments. On the flip side, buyers are demanding deeper due diligence.

Negotiation shifts: Expect robust discussion about filing fees and regulatory cost sharing.

Deal timelines have increased: Early ACCC pre-notification engagement is essential well ahead of filing. Whilst the ACCC is committed to making the regime work and expects to green-light 80% of deals within 15-20 business days, the ACCC can stop the clock on the statutory timeframes (or delay the clock starting). Even simple deals that are notifiable can’t close until around 5 weeks post-filing (factoring in an appeal period).

Higher review risk: The ACCC as the primary decision-maker can escalate deals to a lengthy, costly Phase 2 review if it has competition concerns.

Updated conditions precedent: Modified clearance-related conditions precedent must be integrated into deal documentation that are framed as positive obligations, as well as cooperation obligations and exit rights.

Non-competes: Must be proportionate and necessary to protect goodwill otherwise they risk being declared unlawful.

Gun-jumping risk: A notifiable deal can’t be put into effect until it’s been cleared by the ACCC (or a waiver is granted), so make sure no there’s no integration ahead of this.

Increased challenge risk: There is greater scope for third-party complaints to disrupt deals by triggering reviews of ACCC determinations.

The Addisons Competition/Antitrust & Consumer Team is ready to help you navigate the new merger regime. Contact us for tailored, commercial advice that helps get your deals done.

You can download our current Addisons Merger Control Guide by visiting this link.

Note: This article was originally published on 21 January 2026 but was revised on 1 April 2026 to reflect changes to the thresholds in the new merger clearance regime.

1 This is a question of fact concerning the nature and regularity of the target’s transactions or activities in AU.

2 This is broader than the Corporations Act definition. It means the capacity to determine the outcome of decisions regarding the target’s financial or operating policies, and includes joint control with an associate and control by a special purpose vehicle.

3 The exemptions are detailed and technical. You should seek specific legal advice on whether any exemptions may apply.

4 This is a question of fact and captures asset acquisitions which would enable the acquirer to effectively continue operating a business that is similar to the business currently operated using the acquired assets.

5 If AU revenue of the target > A$2 million, then a 3 year “look back” is required. This captures previous acquisitions by the acquirer group of similar targets > A$2 million, subject to some exceptions.

6 An unlisted body corporate that is not widely held.

7 A Chapter 6 entity (i.e. an AU listed company, listed scheme, or large unlisted company with > 50 members).